Household financial resilience declines in Quarter 1 of 2023, Download the index for further information.

Call us on 010 060 4444 or fill in some quick details and we'll call you.

Altron FinTech’s household resilience index aims to foster greater financial security and prosperity for all, ensuring a stronger and more sustainable future.

Download Presentation

The Index (known as the AFHRI) shows that while household financial resilience increased by 1.4% in the quarter, the decline of 1.1% recorded year-on-year reflects the mounting pressure on household finances.

Background to the AFHRI

In recognition of the need for data that provides more clarity on the financial disposition of households in general, and their ability to cope with debt in particular, Altron FinTech commissioned economist and economic advisor to the Optimum Investment Group, Dr Roelof Botha, to assist in designing this index. The AFHRI comprises 20 different indicators, all related to sources of income or asset values. The AFHRI is weighted according to the demand side of the short-term lending industry and calculated on a quarterly basis, with the first quarter of 2014 being the base period, equalling an index value of 100. All of the indicators are expressed in real terms, i.e., after adjustment for inflation.

Media Release

Altron FinTech releases its Household Resilience Index for Quarter 1 of 2023, showing the decline in SA household financial resilience

Johannesburg, 20 July 2023 – The results of the latest Altron FinTech Household Resilience Index (AFHRI) were released today, indicating that during the first quarter of this year household financial resilience declined by 2.4%, compared to the fourth quarter of 2022 and by 1.8% year-on-year. South African households are now worse off than during the first quarter of 2020, which was pre-COVID-19.

According to Johan Gellatly, the MD of Altron FinTech, the AFHRI continues to provide important information to the company and its customers, as well as consumers in general. “The index assists Altron FinTech to continue enhancing its products and services to assist our customers to differentiate their consumer offering to compete in this highly competitive market segment, no matter the economic circumstances facing the sector, which have been compounded by the systemic decline of continuous electricity supply the country is experiencing. We continuously improve our offerings through intensive research and development, which the data from the AFHRI forms part of. In addition, the AFHRI provides a valuable tool to the sector in terms of benchmarking performance, and this has established Altron FinTech as a thought leader in our field.”

Background to the AFHRI

In recognition of the need for data that provides more clarity on the financial disposition of households in general, and their ability to cope with debt in particular, Altron FinTech commissioned economist and economic advisor to the Optimum Investment Group, Dr Roelof Botha, to assist in designing this index. The AFHRI comprises 20 different indicators, all related to sources of income or asset values. The AFHRI is weighted according to the demand side of the short-term lending industry and calculated on a quarterly basis, with the first quarter of 2014 being the base period, equalling an index value of 100. All of the indicators are expressed in real terms, i.e., after adjustment for inflation.

AFHRI results for the first quarter of 2023 explained

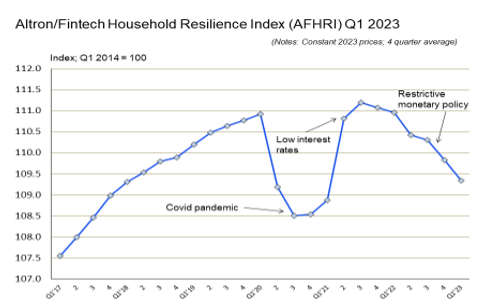

After an initial strong recovery from the effects of the pandemic, which took the AFHRI to a record high in the fourth quarter of 2020, the index remained quite stable until the fourth quarter of 2021, coinciding with the South African Reserve Bank’s (SARB) decision to start raising interest rates. It is clear that higher interest rates have squeezed the finances of most households, with 12 of the 20 constituent indicators of the AFHRI having declined year-on-year and 14 having declined quarter-on-quarter.

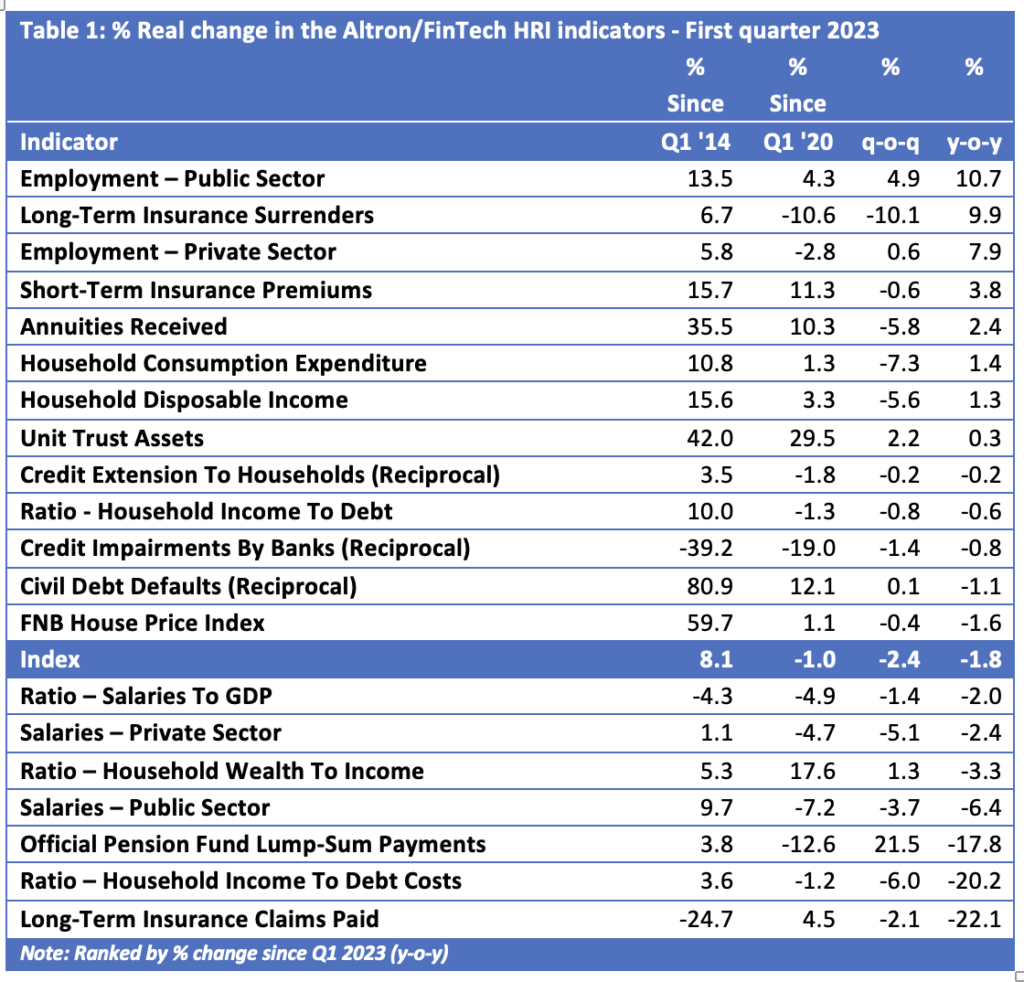

In the first quarter of 2023, the AFHRI recorded a value of 108.1, compared to 110.7 in the fourth quarter of 2022 and 110 in the first quarter of 2022. With a base level of 100 for the inception period of the index (the first quarter of 2014), this means that the average household’s financial disposition has improved by only 8.1% in real terms over a period of nine years. Since 2014, the average annual improvement in the index is less than 1%, which serves as a clear indication of the economy’s under-performance, which has been exacerbated by the negative effects of a sharp increase in the cost of credit. The above graphic illustrates the declining trend on the basis of a four-quarter average, which eliminates seasonal variances. The table below summarises the performance of the different indicators comprising the AFHRI over four different periods, namely since the base period (2014); since the last comparable quarter before the COVID-19 lockdowns kicked in (Q1 2020); as well as quarter-on-quarter and year-on-year (percentage changes in real terms). The period since the first quarter of 2020 is regarded as relevant, in order to gauge whether the financial resilience of households has fully recovered from the pandemic or not.

According to Botha, scrutiny of key constituent indicators of the AFHRI and the reason for the overall downward trend reveals the following:

- The return to restrictive monetary policy by the SARB since the end of 2021 has raised the cost of credit – and of capital – by 68% (as measured against the prime overdraft rate). During the May 2023 meeting of the Monetary Policy Committee of the SARB, the repo rate was raised again by 50 basis points, despite clear indications that both the producer price index (PPI) and the consumer price index (CPI) had already peaked and had entered a decisive downward trend.

- Authoritative commentators that have publicly voiced alarm over the damage caused by excessively restrictive monetary policy include Professor Graham Barr of the University of Cape Town; Professor Brian Kantor of Investec; Tim Cohen, the Business Editor of Daily Maverick; and Samuel Seeff, Chairman of the Seeff Property Group. The consensus view is straightforward, namely that the SARB is placing undue pressure on consumers, businesses and home owners at a time when they are facing several other headwinds, most notably the cost of having to cope with electricity rationing and high energy prices.

- In real terms, total household credit extension, which is valued at more than R2 trillion, has declined by 3.4% since the first quarter of 2014, which means that there has not been any growth in this key macroeconomic indicator over almost a decade. “It is simply not possible for the South African economy to grow at meaningful and sustained rates in the absence of real growth in household credit extension,” says Botha.

Other key conclusions

- On average, the financial resilience of households would have declined by a much larger margin in the absence of a welcome further increase in employment in both the private and public sectors, which represented one of the relatively few bright spots in the first quarter reading of the AFHRI. The upward trend in new job creation continued in the first quarter of 2023, with 258,000 new jobs having been created during the first three months of the year and almost 1.3 million since the first quarter of 2022.

- Unfortunately, the positive employment effect was not matched by total remuneration levels in the economy. The average monthly remuneration in South Africa has declined by 4.4% over the past year (from R16,192 in the first quarter of 2022 to R15,473 in the first quarter of 2023). In real terms (deflated by the consumer price index), the decline was 10.7%.

- Surrenders of long-term insurance policies declined significantly since the fourth quarter of 2022 but remains almost 10% higher compared to the first quarter of 2022.

- During the first quarter of 2023, a sharp decline occurred in the value of long-term insurance claims paid, which could signal the intention of many savers to put their retirement plans on hold until such time as economic conditions start improving.

- Although credit impairments by banks have negatively influenced the AFHRI over all four of the periods under review, this effect has diminished substantially over the past year.

- The strongest indication of the financial pressure on households (induced mainly by higher interest rates) is reflected in the decline of more than 20% in the ratio of household income to household debt costs since the beginning of the year. This trend should be a point of huge concern to government’s economic policy makers outside of the SARB, as it will undoubtedly exert a negative impact on tax revenues and fiscal stability.